Let’s say you’ve just found the perfect job in Toronto. The only problem is that it’s a one-year contract job. You are about to go to a new city, new tasks, and exciting adventures. But who wouldn’t worry about what could go wrong? Now the question is: who would look out for you? This is where short-term health insurance comes in handy. It gives you peace of mind during those short-term changes in your life by acting as a safety net. A lot of Canadians are on or near the edge of change, whether they want to start their own business, get a new job, or just take some time off to travel and study. All of these times are exciting, but they also come with risks and doubts. It’s important to remember that Short-Term Life Insurance is smart and can protect you without committing you to a long-term idea. This choice in Canada will be easier to use if you read real-life stories and get useful advice.

What Exactly is Short-Term Life Insurance?

First things first, let’s get to know Short-Term Life Insurance before we go deeper. Short-Term Life Insurance is just a type of traditional Life Insurance Policy that covers you for a set amount of time, usually years, but may be less than or equal to a few years. It’s meant to help you protect your finances during times of a lot of change or insecurity. Now, let’s take a look at the stories and benefits that have made Short-Term Life Insurance such a popular choice for many.

Advantages of Short-Term Life Insurance

Flexibility to Match Life’s Ebb and Flow

Story: Maria, a freelance web developer in Vancouver, experiences fluctuating income and changing life circumstances year by year. For Maria, the flexibility of Short-Term Life Insurance is invaluable. She can adjust her coverage as her professional landscape shifts, ensuring she’s not overpaying during lean periods.

Advantage: Short-Term Life Insurance matches your current needs without locking you into a decades-long plan. It’s perfect for those who are in transition, whether that’s changing careers, starting a family, or moving internationally.

Affordability When It Matters Most

Story: After graduating, Liam in Montreal found himself burdened with student debt. While he understands the importance of Life Insurance, long-term plans are not feasible. Short-Term Life Insurance offers him an affordable way to ensure his debts are covered, should anything happen to him, without a hefty premium.

Advantage: With generally lower premiums compared to long-term policies, Short-Term Life Insurance is budget-friendly, an essential factor for young professionals and others watching their finances closely.

Fast and Easy to Obtain

Story: When Samantha needed to secure a loan for her new small business in Halifax, the bank requested proof of Life Insurance. A short-term life policy was the quickest solution to meet the bank’s requirements and proceed with her business plans without delay.

Advantage: Short-term policies typically have a straightforward application process with minimal health checks, making it faster and easier to obtain coverage when time is of the essence.

Provides a Safety Net for Your Most Vulnerable Times

Story: Rajkumar, living in Calgary, recently welcomed his first child. While he plans for more comprehensive family coverage in the future, a Short-Term Life Insurance Policy ensures his new family’s immediate financial security as he navigates these early and often unpredictable days of parenthood.

Advantage: During critical life events like the birth of a child, short-term life policy ensures that you’re covered without long-term entanglements, giving you time to plan for the future with more certainty.

Bridge Coverage While Deciding on Long-Term Plans

Story: Emily and John are considering their long-term financial options, including Life Insurance, but they’re not ready to commit just yet. Short-Term Life Insurance serves as a bridge, giving them coverage while they take their time exploring and comparing Term Life Insurance Quotes for a plan that truly fits their long-term goals.

Advantage: Short-Term Life Insurance can act as a placeholder, ensuring continuous protection as you take the necessary time to make informed decisions about long-term insurance commitments.

Integrating Short-Term Life Insurance Into Your Financial Strategy

Having the right tools, like Short-Term Life Insurance, can make all the difference when things go wrong with the money you have. Let’s look at how you can use this flexible type of insurance to protect your finances. We will look at five important ways that Short-Term Life Insurance can help you protect your financial plans.

Covering Immediate Debt Obligations

Real-Life Scenario: Meet Javier, a young entrepreneur from Ottawa who just launched his tech startup. Like many new business owners, Javier took out a loan to cover startup costs. The risk of debt overhang is real, especially in the volatile early years of a business.

Strategy: Javier opts for Short-Term Life Insurance to ensure that if something unforeseen happens to him, his debts won’t become a burden to his family or his new business partners. This coverage is a cost-effective way to manage financial risk without a long-term commitment.

Pro Tip: When comparing Term Life Insurance Quotes, consider how the length of the policy matches your debt repayment schedule. This alignment ensures you’re not paying for unnecessary coverage.

Protecting Your Family During Life Transitions

Real-Life Scenario: Lara and Ben just had their first child and are currently renting in Edmonton. They plan to buy a house soon, adding more financial obligations to their growing family responsibilities.

Strategy: Lara and Ben can protect their family’s future during this transitional phase by using Short-Term Life Insurance. The policy can cover potential financial disruptions caused by any sudden loss of income during critical family growth periods.

Pro Tip: Look for policies that offer flexibility in coverage amounts and terms to adjust as your family’s needs change.

Bridging Gaps Before Long-Term Decisions

Real-Life Scenario: Simran, living in Vancouver, is in a career transition phase and considering several potential paths, including moving abroad.

Strategy: With her future uncertain, Simran uses Short-Term Life Insurance as a stop-gap solution, maintaining coverage while she makes long-term career and life decisions. This approach keeps her covered without the premature commitment to a long-term policy.

Pro Tip: Gather Term Life Insurance Quotes for both short-term and long-term policies to compare costs and benefits. This will help you make an informed decision that matches your career trajectory.

Testing Financial Plans in Real-Time

Real-Life Scenario: Carlos and Anita, a couple from Montreal, are experimenting with different investment strategies to enhance their retirement savings.

Strategy: As they adjust their financial plans, Carlos and Anita utilize Short-Term Life Insurance to ensure their immediate coverage needs are met without hindering their ability to invest and adapt their strategies.

Pro Tip: Consider using Short-Term Life Insurance to cover critical periods while evaluating the success of new financial strategies. This ensures that your risk exposure is minimized during experimentation.

Complementing Employer-Provided Benefits

Real-Life Scenario: Mohan, who works for a tech company in Toronto, receives basic Life Insurance from her employer but feels it’s insufficient given her financial obligations.

Strategy: Mohan supplements her employer-provided benefits with a Short-Term Life Insurance Policy. This additional coverage helps bridge any gaps in her existing policy, especially as she plans for major financial milestones like purchasing a home.

Pro Tip: Assess your current benefits package and determine if adding Short-Term Life Insurance could provide the extra security you need. This is particularly important during major life events or financial undertakings.

Understanding and utilizing the Short-Term Life Insurance advantages can significantly contribute to your financial resilience. Each of these strategies provides a practical framework for integrating Short-Term Life Insurance into your financial planning. Whether you’re covering debts, protecting your family, or bridging gaps in coverage, Short-Term Life Insurance offers a flexible and targeted approach to safeguarding your financial well-being.

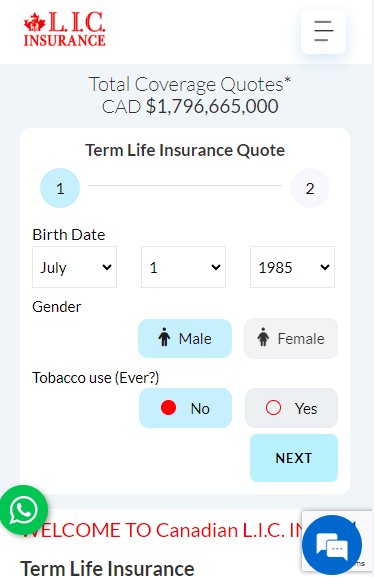

Remember, life is full of changes, and having adaptable financial tools at your disposal can help you manage these transitions more smoothly and securely. If you’re considering adding Short-Term Life Insurance to your financial toolkit, compare Term Life Insurance Quotes and explore the best options tailored to your unique life situations. Engage actively with your insurance decisions—it’s not just about having coverage; it’s about having the right coverage right now.

| Feature | Short-Term Life Insurance | Long Term Life Insurance |

|---|---|---|

| Duration | Coverage typically lasts from 1 to a few years. | Coverage can last from 10 years to a lifetime, or even up to a specific age. |

| Cost | Generally lower premiums due to shorter coverage period. | Higher premiums due to longer coverage and often more comprehensive benefits. |

| Flexibility | High flexibility to change or cease coverage as personal circumstances change. | Less flexibility; intended for long-term financial planning and stability. |

| Coverage Purpose | Ideal for temporary needs, such as covering a loan or short-term debt. | Suited for long-term needs like family protection or estate planning. |

| Renewability | Often renewable at the end of the term, sometimes with adjusted terms. | May offer guaranteed renewability or convertibility into permanent coverage. |

| Underwriting | Simpler underwriting process, often with fewer health examinations. | More extensive underwriting, possibly requiring detailed medical exams. |

| Benefit Amount | Typically lower benefit amounts compared to long-term policies. | Higher benefit amounts to support dependents, pay off debts, etc. |

| Ideal For | Individuals in transition, needing temporary coverage. | Individuals seeking stability and long-term financial security. |

Conclusion: Taking Action Right Away

In a lot of situations, Short-Term Life Insurance works out really well, is easy to change, and is reasonably priced. In fact, it is ideally catered to the most dynamic lifestyles and transient periods that form so much of modern life in Canada. If you find yourself in a place where the future feels tenuous, or you find yourself in a state of significant life changes, think about how Short-Term Life Insurance might work as your money safety net. Don’t leave yourself vulnerable to the unknown. Contact us today to see how Short-Term Life Insurance fits into your life and assures your peace of mind. Remember, now is the right time to secure your future, so take that step toward a Term Life Insurance plan or a traditional Life Insurance Policy appropriate to your current phase of life and see how it can transform your approach toward both financial security and resilience.

Find Out: The main disadvantage of Term Life Insurance

Find Out: Do Term Life Insurance rates go up?

Find Out: How do you choose Term Life Insurance?

Find Out: Do you get money back from TermLife Insurance?

Find Out: The reason to get Term Life Insurance

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs: Short-Term Life Insurance in Canada

Short-Term Life Insurance offers a few main advantages: affordability, flexibility, and ease of qualification. For instance, consider the story of Nadia from Quebec City, who found herself between jobs and needed a temporary insurance solution. She took a Short-Term Life Insurance Policy because it is the only affordable means of insurance, and it offers a flexible solution to ensure that she is fully covered during this transitory period until she has secured another full-time role with comprehensive benefits.

Gather some offers from multiple insurance firms to compare and get the best quotes for Term Life Insurance. Get online quotes, go to insurance agents directly, or use comparison tools. Kamlesh from Saskatoon got quotes from three different companies and compared each of them in terms of cover terms and premium costs to finally pick one for his short-term needs.

Yes, some Short-Term Life Insurance policies offer the option to convert to Long Term Life Insurance without further medical exams. This has been a lifesaver for Aisha in Halifax, who first took the short-term plan at a time when she didn’t have much money. As soon as she managed to turn things around, she converted the coverage to a Long Term Life Insurance Policy to make sure her family was protected.

When going in for a Short-Term Life Insurance Policy, consider the sum assured, premium cost, term length, and flexibility of renewing or converting the policy. Consider the case of Raj from Calgary, who availed himself of a renewable policy since he was in a state of confusion, not knowing if he would require the longer length of coverage at such an early stage of his career. It gave him enough flexibility to extend the coverage if needed.

For a person with a family, it can be a Life Insurance that helps at times of great change or uncertainty, especially when life is short. For example, Emily in Toronto, who was already on maternity leave, chose a Short-Term Life Insurance Policy to add to the financial protection of her family during this vulnerable time. This enabled her to return to work with the peace of mind to reassess her long-term insurance needs.

The other reason why Short-Term Life Insurance often quickly processes is that there are no complicated underwriting processes. For example, in Edmonton, Mark was able to procure a policy just within a few days after application, which he said was very critical since he needed the coverage right away before starting a new and quite risky venture. This really helps those people who urgently need this coverage.

The cost of Short-Term Life Insurance is based on numerous factors, such as the policyholder’s age and health, the value of the coverage, and the term of the policy. For instance, Alex in Brampton learns that, by any standards, his premiums were pretty low since he was young and in very good health. It’s important to understand that your personal circumstances will play a significant role in determining your premium.

Yes, most Short-Term Life Insurance policies can be renewed when they reach the end of their terms. Lisa from Vancouver, for example, had an initial one-year policy when she started freelancing. As her career took off, she continued to renew the policy each year, modifying the coverage amount to fit what she needed for her business. Be sure to ask about the details of the renewal policies and if the premium can change upon the renewal.

Broadly speaking, Life Insurance premiums, including Short-Term Life Insurance, are not tax-deductible in Canada. However, by general rule, the beneficiary’s benefit upon the policyholder’s death is received tax-free. This greatly relieved Tom from Montreal, for his beneficiaries received the payout without deduction, which really fully supported them in a challenging time.

The amount of coverage you buy will depend on your current financial obligations and the extent of financial security you would like to leave to your beneficiaries. For instance, Julie, from Winnipeg, determined an amount of coverage needed to repay her debt and leave some level of financial leverage for her children. It would be best if, in consideration of that, you re-evaluate your financial position carefully and even probably consult with a financial advisor on how much coverage is appropriate.

Life Insurance provides a death benefit for beneficiaries in the event the insured loses their life, while health insurance covers medical care costs like doctor’s appointments, hospital stays, and prescriptions. Michael in Calgary did, in fact, have both insurances. He used his health insurance to manage his medical expenses after he had an accident, and his Short-Term Life Insurance was there to serve as a safety net for his family if the worst was to happen.

Yes, Short-Term Life Insurance is available to individuals with pre-existing health conditions. Terms and premiums would vary depending on the seriousness and nature of the condition. For example, Sarah of Toronto was able to secure a short-term policy for a chronic condition after her insurance company considered detailed medical records and a medical assessment. The downside is, of course, that you might have to pay higher premiums and limit the coverage you can get, so it really does pay to shop around and compare Term Life Insurance Quotes to find the best deals.

Knowing the answers to these common questions will guide you, and understanding the real-life situations others have shared, you will find your way through the maze of Short-Term Life Insurance, making it all the more conducive to picking an informed decision that fits your current life situation. Take your time to review your options always, and settle for what best suits your needs and circumstances.

Sources and Further Reading

To deepen your understanding of Short-Term Life Insurance and help guide your decisions, here are some recommended sources and further reading materials. These resources provide comprehensive insights into Life Insurance options in Canada, helping you navigate the complexities of insurance products and make informed choices.

Financial Consumer Agency of Canada (FCAC)

Website: Canada.ca

Why visit: The FCAC offers detailed guides on different types of insurance available in Canada, including Life Insurance. Their resources are invaluable for understanding the regulatory and practical aspects of financial products.

Insurance Bureau of Canada

Website: IBC.ca

Why visit: This site provides insights into insurance coverage options, industry news, and helpful tips on choosing the right insurance policy for your needs.

Canadian Life and Health Insurance Association (CLHIA)

Website: CLHIA.ca

Why visit: The CLHIA offers resources on life and health insurance products and is a great source for learning about insurance trends and standards in Canada.

Investopedia: Life Insurance

Link: Investopedia – Life Insurance

Why visit: Provides a broad overview of Life Insurance, including different types of policies and what factors you should consider before purchasing insurance.

NerdWallet: How to Get Life Insurance Quotes

Link: NerdWallet – Life Insurance Quotes

Why visit: This guide explains how to effectively compare Life Insurance quotes and what you should look out for in a policy.

Key Takeaways

- Short-Term Life Insurance offers flexibility and convenience for individuals in transition.

- It is generally more affordable than long-term insurance, suitable for those on a budget.

- The application process is typically straightforward and fast, allowing for quick coverage.

- Serves as an excellent interim solution while making permanent long-term insurance decisions.

- Can be tailored to meet specific, short-term financial obligations.

- Acts as a vital risk management tool that adjusts to changing personal circumstances.

- Is a strategic component of financial planning to protect against unforeseen challenges.

Your Feedback Is Very Important To Us

The responses to this questionnaire will help identify common struggles and areas for improvement in the marketing and structuring of Short-Term Life Insurance policies, aiming to better meet the needs of Canadians.

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to [email protected] or [email protected]