Need help with Whole Life Insurance? You’re not alone. Many Canadians scratch their heads when they hear terms like “paid-up additions”. You’re planning for your financial future, and you come across different options, each with its own intricacies. That’s where we come in. Today, we’re going to break down one of those components – paid-up additions – that can add big value to your Whole Life Insurance Policy. Whether you’re a young professional just starting out or a seasoned investor looking to diversify your portfolio, understanding paid-up additions can be a game changer for you.

Understanding Paid-Up Additions

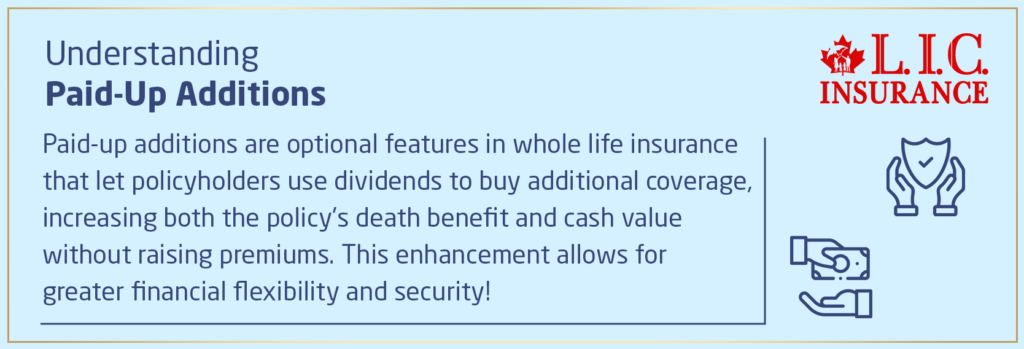

What Exactly are Paid-Up Additions?

Paid-up additions are miniature life insurance policies that provide for the same death benefit and cash value as regular life insurance policies but do not require continuous premiums after the initial upfront payment. They are purchased using life insurance dividends from a Whole Life Insurance Policy, which allows a policyholder to increase coverage and cash value without increasing regular out-of-pocket costs.

John, a Canadian LIC client, shared how the inclusion of PUAs was not an option but a well-thought-out strategy in his policy. Initially skeptical, John realized through detailed discussions with his advisor how these inclusions enhanced the value proposition of his policy. This was more important since he had plans to educate his children and leave behind a robust financial legacy.

Benefits of Paid-Up Additions

Increased Insurance Coverage and Cash Value

The first benefit that including PUAs in your Whole Life Insurance Policy can have is that, once added, they immediately increase the policy’s death benefit and its cash value. That growth is tax-deferred and may compound, which gives you a huge advantage in long-term wealth accumulation.

Flexibility in Premium Payments

The following is one of the flexible ways PUA offers for you to remit your Whole Life Insurance Premium: you can decide at what time and amount to contribute, hence setting it against financial conditions and goals of the time. Flexibility is critical in case one has fluctuating income streams or other uncalculated expenses.

Sheeba, another Canadian LIC client, utilized PUAs to adjust her premium payments during a year when her freelance business saw unexpected downturns. This flexibility allowed her to maintain her policy and even grow its value during challenging times.

How to Utilize Paid-Up Additions Effectively

Regular Reviews with Your Advisor

In order to make the most out of PUAs, it’s essential to review your Whole Life Insurance Policy with your advisor regularly. This ensures that your additions align with your changing financial goals and market conditions.

Consider Your Long-Term Financial Goals

The overall financial planning that uses PUAs should integrate clearly defined long-term objectives. These could pertain to funding retirement, funding for healthcare in later years of life, or leaving a legacy. PUAs can be structured to fulfill any or all of those objectives.

Mark and Linda, a couple in their mid-50s, decided to boost their retirement savings by leveraging PUAs. Their advisor at Canadian LIC helped them understand how these additions could secure a more comfortable and financially stable retirement.

Common Misconceptions About Paid-Up Additions

“They Are Too Complicated to Understand”

Many believe that PUAs are too complex. However, with the right guidance from a knowledgeable advisor, they can be a straightforward and powerful addition to your financial toolkit.

“Only Wealthy Individuals Can Afford Them”

While it’s true that PUAs require additional investment, they are accessible to a wide range of clients. The key is starting early and consistently reviewing your financial capacity to contribute.

Emily, a young professional, initially thought PUAs were beyond her reach. However, after consultation with Canadian LIC, she started small and gradually increased her contributions as her career advanced.

How to Purchase Paid-Up Additions

Buying PUAs can, however, be simple if one knows what their policy states and how the dividends are payable. Here’s how you can go about it:

Step-by-Step Guide

Review Your Policy: Understand how dividends are paid and if they can be used to purchase PUAs.

Consult Your Advisor: Discuss with your Canadian LIC advisor how best to use your dividends for PUAs based on your financial goals.

Reinvestment Decision: Opt to reinvest your dividends into PUAs, enhancing both the death benefit and cash value of your policy.

Making the Right Choice

Lina, advised by her Canadian LIC consultant, decided to use her dividends for PUAs after a thorough review of her financial goals and insurance needs. This decision was pivotal in maintaining her lifestyle after retiring.

Conclusion: Why Choose Canadian LIC?

Choosing Whole Life Insurance with paid-up additions through Canadian LIC is not just about getting a policy; it’s about creating a plan that grows and evolves with your life stages. Canadian LIC’s personalized approach ensures that each client gets the right balance of coverage for their needs and beyond.

Don’t wait for the perfect moment to boost your financial security. The time is now, and the place is Canadian LIC. Get in touch with us today to see how we can design a Whole Life Insurance solution for your unique life and secure your future.

More on Whole Life Insurance

Are There Any Circumstances Under Which The Death Benefit Of Whole Life Insurance Would Not Be Paid?

What Is The Impact Of Smoking On Whole Life Insurance Premiums?

Can I Adjust My Whole Life Insurance Policy?

How Is The Cash Value Of A Whole-Life Policy Taxed?

How Can You Find The Best Whole Life Insurance Without A Medical Exam?

What Age Does Whole Life Insurance End?

What Are The 2 Disadvantages Of Whole Life Insurance?

At What Age Is Whole Life Insurance Good?

Can I Buy Whole Life Insurance For My Child?

Who Should Opt For Whole Life Insurance?

Is Whole Life Insurance Expensive?

Understanding How Does A Whole Life Insurance Policy Work: A Comprehensive Guide

What Is The Biggest Risk For Whole Life Insurance?

What Is The Difference Between Money Back Policy And A Whole Life Policy?

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

FAQs on Paid-Up Additions in Whole Life Insurance

Paid-up additions are small, fully paid portions of life insurance that increase both the death benefit and the cash value of your Whole Life Insurance Policy. Consider this: You’re much like Tim, a Canadian LIC client who wanted his policy to grow but was concerned about his budget. Using his dividends to buy paid-up additions effectively increased Tom’s coverage without raising his ongoing Whole Life Insurance Premiums.

Good question! The dividends that accrue on the existing Whole Life Insurance Policy can be used to buy additional paid-up insurance, which means there is nothing you have to pay extra from your pocket. Maria was a client at Canadian LIC and found this method to be perfect. It fits quite well with her goal of increasing coverage without straining her budget by paying high premiums monthly for the whole life policy.

Absolutely! These paid-up additions to your Whole Life Insurance Policies add to your cash value, which grows over some time and is available if you need to borrow. For example, David from Canada utilized the cash value of his paid-up additions to fund a down payment on a new home.

For a quote about Whole Life Insurance with paid-up additions, contact Canadian LIC. We will provide you with a custom quote showing how the addition of paid-up additions is going to enrich your policy. When Leema contacted us for a quote, she was pleasantly surprised to learn how very affordable it can be to add paid-up additions as part of her financial planning.

While paid-up additions offer many benefits, some might have better choices. It all depends on your financial goals and where you are in the process. Jammy, one of our clients with Canadian LIC consultation, felt it was more suitable for his short-term financial needs to focus his dollars on his current Whole Life Insurance Premiums. We invite you to consult with a Canadian LIC advisor to determine whether this is the right option for your personal financial strategy.

If you opt to surrender the whole of your life insurance policy, then the cash value of paid-up additions is added to the surrender value. This had been an important consideration for Samantha, who had an urgent need for liquidity, which she discovered was substantially enhanced by the cash she had accumulated through her paid-up additions, thus enabling her to receive the much-needed funds at the time.

Yes, you can start the paid-up additions at any time, provided your policy allows for it and you are receiving dividends. Robert started his policy without a paid-up addition. He decided to bring in the paid-up addition after five years, which added more value to the policy as his financial situation improved.

Paid-up additions are purchased using dividends from your Whole Life Insurance Policy, which means that no additional premiums are required. This was a game-changer for Anita, a Canadian LIC client who had been concerned at first by the cost earlier. She felt relieved by the fact that she could increase her coverage without changing her monthly budget committed to Whole Life Insurance Premiums.

Before opting to have paid-up additions, first consider your long-term financial goals and current financial condition. Neil is among the experienced Canadian LIC advisors who consistently share stories like his client Ben, who considered the possible income he would earn in the future and his retirement plans as a way of deciding whether investing in paid-up addition was the right thing to do. It’s vital to discuss it with a professional so that this feature will be tailored based on your needs.

You can buy paid-up additions as often as you receive dividends from your Whole Life Insurance Policy, which is usually annually. Chloe, one of our clients, annually reviews how her policy is performing and whether or not to reinvest her dividends in paid-up additions. This helps to keep the growth of her Whole Life Insurance Policy aligned with her changing financial priorities.

Paid-up additions to one’s current policy may not directly impact the quotes one can receive for a second policy. However, the ability to showcase an up-to-date and financially healthy current policy can sometimes lend a positive flavour to views concerning your financial stability. In Kevin’s case, advisors from Canadian LIC were using his well-managed first policy as an example of his excellent financial acumen, which helped him attract better terms for the second policy.

Growth in cash values in the form of paid-up additions through a Whole Life Insurance Policy is generally tax-deferred under Canadian law. Thus, different situations may mean different things, especially if you are withdrawing from or borrowing against such a policy. Canadian LIC helped a client, Susan, understand these implications to ensure she makes the most of her policy without unexpected tax repercussions.

Annual statements are sent out by Canadian LIC, detailing how your Whole Life Insurance Policy is performing. This allows clients like Omar—a careful watcher of his investments—to know exactly how his decisions shape the growth and security of his policy.

Once added, paid-up insurance additions normally cannot be removed as single items from a policy since they become part and parcel of your Whole Life Insurance coverage. This was important for her to know since Saba initially thought that she could opt in and out of a savings account. Advisors from the Canadian LIC ensure that their clients understand that such features are long-term enhancements to their policies.

Consider these FAQs and how the decisions of some of our clients—have played out to get a clearer view of how paid-up additions might work to help strengthen your Whole Life Insurance plan. Remember, Canadian LIC is here to ensure that you will make the decision that is best for you. Feel free to reach out to our financial advisor with more questions or for a detailed quote!

Sources and Further Reading

Life Insurance Basics – Investopedia

A comprehensive guide covering the fundamentals of life insurance, including the types of policies and features like paid-up additions.

Investopedia: Life Insurance Basics

Understanding Whole Life Insurance – NerdWallet

This article provides an in-depth look at Whole Life Insurance, with a focus on premiums, cash value accumulation, and dividends.

NerdWallet: Understanding Whole Life Insurance

Whole Life Insurance: How to get It – Forbes

Forbes offers a practical perspective on when and why to use Whole Life Insurance, including strategies for incorporating paid-up additions.

Forbes: Whole Life Insurance: How to get It

Canadian Life Insurance Guide – Canada.ca

The official Canadian government resource on life insurance policies, providing legal and practical information relevant to Canadian citizens.

Canada.ca: Canadian Life Insurance Guide

How Dividends Work With Whole Life Insurance – The Balance

An article explaining how dividends are generated in whole life policies and how they can be used to purchase paid-up additions.

The Balance: How Dividends Work With Whole Life Insurance

These resources will provide you with a solid foundation of knowledge on Whole Life Insurance and paid-up additions, complementing the information shared in our blog.

Key Takeaways

- Paid-up additions let policyholders use dividends to buy extra coverage without increasing premiums, enhancing both death benefit and cash value.

- This feature offers financial flexibility by enhancing insurance coverage and building cash value without straining personal budgets.

- Paid-up additions increase a policy's death benefit and cash value while providing tax-deferred savings accessible during the policyholder’s life.

- Canadian LIC offers personalized advice to help determine if paid-up additions suit individual financial goals and needs.

- These additions contribute to long-term growth and security, making Whole Life Insurance a more effective financial planning tool.

- Readers are encouraged to consult with professionals like those at Canadian LIC for tailored advice and Whole Life Insurance Quotes.

Your Feedback Is Very Important To Us

We appreciate your feedback! This questionnaire aims to understand the specific challenges you face with paid-up additions in your Whole Life Insurance Policy. Your responses will help us improve our services and provide more relevant information.

Please submit your responses using the provided options or feel free to add any additional comments you might have. Thank you for helping us better understand and serve your insurance needs!

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to [email protected] or [email protected]