- Connect with our licensed Canadian insurance advisors

- Shedule a Call

BASICS

COMMON INQUIRIES

- Can I Have Both Short-Term and Long-Term Disability Insurance?

- Should Both Husband and Wife Get Term Life Insurance?

- Can I Change Beneficiaries on My Canadian Term Life Policy?

- What Does Term Life Insurance Cover and Not Cover?

- Does Term Insurance Cover Death?

- What are the advantages of Short-Term Life Insurance?

- Which Is Better, Whole Life Or Term Life Insurance?

- Do Term Life Insurance Rates Go Up?

- Is Term Insurance Better Than a Money Back Policy?

- What’s the Longest Term Life Insurance You Can Get?

- Which is better, Short-Term or Long-Term Insurance? Making the Right Choice

IN THIS ARTICLE

- Can I Transfer Money To RRSP Online?

- Getting a Registered Retirement Savings Plan Quote Online

- Comparing Registered Retirement Savings Plan Providers in Canada

- Registered Retirement Savings Plan Providers in Canada-Comparison

- Step-by-Step: How to Transfer Money to an RRSP Online

- Advantages of Transferring Money to an RRSP Online

- Take Action Today for Peace of Mind

- Challenges and How to Overcome Them

- Conclusion: Is Transferring Money to an RRSP Online the Right Choice?

Can I Transfer Money To RRSP Online?

By Pushpinder Puri

CEO & Founder

- 11 min read

- February 27th, 2025

SUMMARY

This blog guides you through transferring money to your RRSP online, highlighting key steps, security tips, and common mistakes to avoid. It discusses different RRSP providers in Canada, including banks, credit unions, and online brokers, and explains how to choose the right one. The blog also covers how to get a Registered Retirement Savings Plan Quote Online, offers tips on avoiding contribution penalties, and compares online transfers with in-person banking.

Introduction:

Sarah, a 35-year-old from Toronto, sat down one evening with a cup of coffee and a firm goal to invest in her future. She knew that opening and contributing to a Registered Retirement Savings Plan (RRSP) was a good way to prepare for her retirement, but the thought of transferring money online to an RRSP just made her nervous. Would she hit the wrong button and make an error? Could somebody get her information? And there were so many banks and financial companies out there offering RRSPs; how could she possibly find the right one? Sarah is not alone in feeling this way. For many of our clients at Canadian LIC, these kinds of questions have echoed over the years as they navigated their way through RRSP contributions online. In fact, many of them have gone so far as to search for a “Registered Retirement Savings Plan Quote Online,” similar to purchasing a simple insurance product, and were even more confused than ever about all the options available.

The real-life questions, even the fear of being wrong, the anxiety about online safety, and confusion over how to select among Registered Retirement Savings Plan Providers in Canada are super common. The good news is that, with some guidance and education, those fears can transform into confidence. This blog will take you through Sarah’s (and possibly your) journey from the anxious start to a comfortable, step-by-step understanding of how to transfer money to an RRSP online. In the process, we’ll discuss the benefits of transferring money online, the things to look out for, and how to make the transaction as seamless and safe as possible.

Are you ready to take this journey with Sarah? Let’s tackle one of her initial big questions: Where do I start?

Getting a Registered Retirement Savings Plan Quote Online

When Sarah initially made up her mind to invest in an RRSP, she did what we all tend to do – she went to Google. She entered “Registered Retirement Savings Plan Quote Online” in a hurry to get the best RRSP quote. It’s a term we commonly hear from clients who are approaching an RRSP as they would a car insurance policy or a term life plan, looking for a quick quote. The truth is a little more complicated. An RRSP is not a one-product, fixed-price item; it’s an account that can contain different investments (such as savings deposits, mutual funds, stocks, or GICs). So, though you won’t get a quote for an RRSP, there isn’t a one-size-fits-all solution; online searching is still an excellent way to compare your choices.

Rather than an easy quote, what you find on the net are calculators and tools that will assist with determining how much you may be required to set aside or how much you may receive back in tax refund from donating so much. Take Sarah, who discovered an RRSP contribution calculator that indicated what she could expect in tax savings if she put in $5,000 for this year. More significantly, she discovered comparison pages with various RRSP accounts and their attributes – sort of like getting a quote by comparing fees and interest rates. If you encounter the phrase “RRSP quote,” it generally refers to comparing these attributes or obtaining an investment quote (such as the prevailing interest rate on an RRSP savings account or the management fee of an RRSP mutual fund).

The takeaway? Don’t stress if you can’t discover a single “price” for an RRSP. Take advantage of the online browsing experience to learn. Search for RRSP interest rates, investments, and customer feedback. Numerous financial institutions in Canada offer details online where you may input your information and view estimates for your retirement savings – this is effectively the essence of requesting a quote for your RRSP savings. Sarah understood that rather than looking for a single quote, she should compare multiple quotations to determine what best fit her. That leads us to the next step of her process: selecting the appropriate provider.

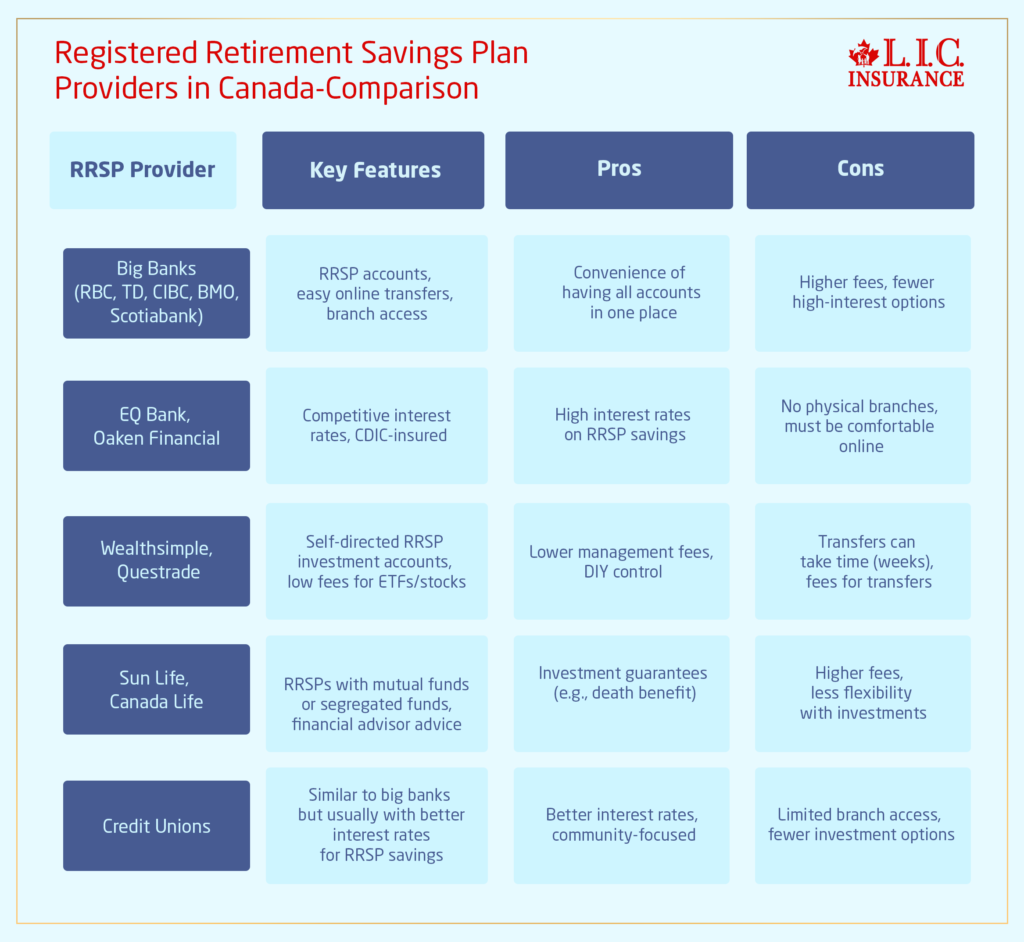

Comparing Registered Retirement Savings Plan Providers in Canada

With the long queue of banks, credit unions, insurance firms, and online investing services to navigate through, Sarah got confused. The Canadian ground offers a thick culture of RRSP providers, and one seems to assure something better. Actually, it is possible to establish a Registered Retirement Savings Plan with practically every kind of financial institution – trust companies, credit unions, insurance companies, and banks all make a profit in selling RRSP accounts

. With so many choices, the question becomes: how do you choose the right RRSP provider for your needs?

Let’s break it down. Big banks are a popular option. Providers such as RBC, TD, CIBC, BMO, and Scotiabank all have RRSP accounts and make online money transfers simple through their banking sites.

If you already bank at a large bank with a chequing or savings account, the convenience of having all your accounts in one location can be a significant advantage. Sarah, for example, was inclined towards her current bank (TD) merely because she was comfortable with their online banking.

Aside from banks, there are credit unions and online banks with better interest rates on RRSP savings. EQ Bank or Oaken Financial may be mentioned – these online banks can have excellent rates and are equally secure (EQ Bank, for instance, is CDIC-membered and has competitive RRSP savings rates)

The drawback is that they don’t have physical branches, so you need to be okay with doing everything online or through an app. Sarah took this into account when she noticed a good rate at an online bank; the prospect of getting a little more interest was appealing.

Online venues such as Wealthsimple or Questrade enable you to start an RRSP investment account yourself online and often charge lower rates for buying into ETFs or stocks. If you’re not opposed to trying it on your own or liking the app-only experience, those are solid. Wealthsimple also has deals (like they match part of your transfer) that encourage you to transfer over your RRSP

But moving an existing RRSP from one organization to another can be a waiting game (occasionally weeks) and costs money (in some cases $50–$150, which some companies will absorb to gain your account)

Insurance firms provide RRSPs, typically mutual fund or segregated fund policies. Sun Life and Canada Life sell RRSP investing, which is often packaged with a financial adviser’s advice. If you wish to have a guiding hand along with perhaps the inclusion of something like investment guarantees (in segregated funds), you might find them interesting. Canadian LIC, being a brokerage for insurance and investments, can frequently assist clients in making sense of these alternatives. For instance, one of our clients elected to have a segregated fund RRSP with an insurer because he preferred the death benefit guarantee option over his retirement funds – something usual bank RRSPs do not provide.

So how did Sarah choose? She put her priorities into a list. She desired ease of use, robust security, fair fees, and the ability to speak to someone if she needed support. She knew that whichever federally regulated provider she used would be secure – banks and credit unions belong to the Canada Deposit Insurance Corporation (CDIC), which ensures deposits and investment accounts are insured by the Canadian Investor Protection Fund (CIPF) against broker failure. With security taken care of, it was a matter of convenience. Ultimately, Sarah decided to remain with her bank for the time being, aware that she could switch later. The comfort of the online banking site prevailed, and she created an RRSP investment account there (it took her approximately 10 minutes to complete the application online).

With her RRSP account in hand, the real challenge was then transferring her money into it. Now came the moment of truth – moving money online, for the first time, into her own RRSP.

Registered Retirement Savings Plan Providers in Canada-Comparison

Step-by-Step: How to Transfer Money to an RRSP Online

Log into your online banking or investment account: Go to the web or app for the financial institution that holds your RRSP and log in. For Sarah, she logged into her bank’s online portal and saw all her accounts (chequing, savings, now an RRSP) were listed on the dashboard. Enter this information (but only) over a secure internet connection (avoid public Wi-Fi at this step) to protect your information.

Go to your RRSP account: From the dashboard, go to your account list and click on your RRSP. Many NJ online banking login platforms have a separate section for investment or retirement accounts. In RBC’s online banking, for example, you would go to the Accounts Summary page, click on your RRSP account, and select the Contribute option.

Sarah had taken the same steps but had clicked her new RRSP account from her TD online banking homepage, and it opened options to manage that specific account.

Select method of payment: Specify which account the money will come from. Usually, you’ll transfer from a chequing or savings account directly into the RRSP. Sarah picked her chequing account as the source because that’s where her paycheque is deposited. If your RRSP is at a different institution than your bank, you might need to add the RRSP provider as a payee (same as paying a bill) or set up an electronic funds transfer. Most deposits into investment RRSP providers (like Questrade) can be funded by linking your bank account or even via Interac e-Transfer.

Enter contribution amount: This is where Sarah stepped back to compare her figures. She recalled that there are yearly dollar limits to RRSP contributions. She confirmed her current RRSP contribution room for the year based on her Notice of Assessment from her last tax return. (Also, she hadn’t maxed out previous years, so she had lots of room to move. You need to check your limit — exceeding your limit by more than $2,000 will result in a penalty of 1% per month on the contribution in excess of your limit.

Tip: If you’re uncertain, you can find your contribution limit in the Canada Revenue Agency’s My Account portal or in the paper notice mailed after you file taxes.

Double-check the details: After Sarah entered, say, $5,000 as a contribution and checked “Next,” she reviewed the summary. The screen displayed all the information: the from account (her chequing) and the to account (her RRSP), the amount and the date (she did it right away). She checked that everything looked good — no stray zeros in the amount by accident! We always advise clients at this point: take time to reflect. It’s a lot easier to fix a typo now than after you press submit.

Finalize the Transfer: Sarah clicked on the “Confirm” or “Submit” button, sending the transfer off with a deep breath. And a caption later, the transfer was complete! In one second, she looked to see the balance in her RRSP account reflect the new contribution. Most electronic transfers to an RRSP occur immediately if you are dealing with the same bank. When moving funds into an RRSP at another institution, it can take 1-2 business days for the money to show up (or longer if you are doing a formal transfer from an existing RRSP between institutions, a process that involves filling out some paperwork). Sarah’s transfer was made through her own bank, so the update was instant.

Save the confirmation receipt: After completing the transaction, she downloaded the confirmation page as a PDF file and wrote the transaction ID down. The other fact that she had in her mind was that her bank was going to produce an official RRSP contribution receipt (for tax purposes) around the year-end or early March for any contributions made within the first 60 days of the year. Record-keeping is important, especially because if you give in January or February for the previous tax year — those are your tax receipts.

Invest the contribution (optional next step): Putting cash into an RRSP is only half the equation. What should we do with that money afterwards? In Sarah’s case, she had made contributions to a self-directed RRSP investment account. That meant her $5,000 sat as cash in the RRSP. Her strategy was to put it into a balanced mutual fund in the RRSP. So the last step was for her to order — she could also do it on the internet — purchasing units of the mutual fund with that cash. If your RRSP is just a savings deposit, you can probably skip this step — your funds may be already accruing interest. But if it’s an investment account, keep in mind that contributing is only Step 1, after which you need to invest the money according to your plan so it can grow.

Following these steps, one at a time, Sarah made her first online RRSP contribution without a hitch. She even signed up for a pre-authorized contribution for after – a service whereby the bank will direct deposit a predetermined portion from her chequing to her RRSP monthly. This “pay yourself first” method meant she wouldn’t need to repeat the manual steps every single time, and it’s a tactic that’s particularly helpful for many to ensure they remain on-target with their retirement savings (banks stress that on-time, regular automatic contributions to your investment portfolio are a positive thing).

Having done it, Sarah was relieved and even proud. The once-daunting experience was empowering. But she also picked up a few tips on the ups and downs of doing it the way she did. Let’s examine the upsides she uncovered and the downsides she overcame by transferring money to her RRSP online.

Advantages of Transferring Money to an RRSP Online

After submitting her online transfer, Sarah was soon able to see why so many Canadians are choosing to handle their own RRSPs online. Based on Sarah’s experience and other Canadian LIC clients, here are some key benefits to doing an online transfer of funds to your RRSP:

Convenience Convenience and Access: Number one, We think. You can make your RRSP contribution anytime, anywhere. You do not have to go to a bank branch or mail a cheque. As long as you have internet access, you can plan for retirement at your fingertips. Online banking offers up to “convenience and accessibility,” enabling you to manage accounts and perform transactions from the comfort of your home or on the go. For people strapped for time or people who live far from the nearest brick-and-mortar bank, it will be a lifesaver.

Speed and Timeliness: One of the primary advantages of online transfers is their speed. Suppose you suddenly discover the RRSP contribution deadline (the 60-day deadline for contributions to count in last year’s taxes) is tomorrow. In that case, an online transfer can be done in seconds — mailing a cheque or setting an appointment may simply take too long. One thing Sarah loved was that her contribution had an instant impact. And you also receive instant confirmation, which is helpful when time is of the essence.

Fewer Error (with Immediate Feedback): To Sarah’s surprise, putting it online actually made her less afraid of making a mistake. Why? The interfaces typically catch common errors (such as leaving an amount field empty) and will always confirm a transaction. It’s more difficult to, for example, write an additional zero like you can on a paper form without it appearing on screen. And if you do screw up, you’ll usually catch it immediately during confirmation. Some even warn you if a transaction would exceed a limit, but you shouldn’t count on that.

The takeaway: The concise directions and summaries available online can help you steer clear of missteps.

Security: It may sound counterintuitive, but online transfers can be highly secure. Banks and finance institutions deploy encryption and multi-factor authentication to secure transactions. When you move money in a secure online session, that transaction is encrypted from end to end. No physical papers to lose or steal or be lost or stolen. And any trusted, regulated institution would do so with safety nets like deposit insurance. Funds in a regular bank RRSP savings account, for example, are typically CDIC-insured (up to $100,000) as is any other bank deposit — which is an additional peace of mind. Even most banks will guarantee your protection: if someone makes an unauthorized transaction, you just report it, and they’ll investigate and compensate you, assuming you took reasonable care (keeping your password secure, etc.).

To Sum It Up: As long as you practice good online hygiene, online RRSP transfers are very safe.

Easily Found and Managed: Online access lets you check your RRSP balance, confirm your contribution history, and even reallocate investments in real-time. Most platforms will allow you to establish alerts (for example, receive an email or text every time a contribution goes through or when your account balance reaches a specific level). This transparency can provide peace of mind and a sense of control. For example, whenever Sarah’s automatic monthly contribution was deposited into her RRSP she set an alert to notify her, so she could always rest assured knowing it was taken care of. Watching your nest egg grow with each transfer is satisfying, and having that information at your fingertips can encourage you to persevere.

Potential for better rates or promotions: Certain providers may offer incentives for those who use online services. For example, a high-interest online RRSP savings account can return you a much better return than a traditional account at a physical bank. Also, there are specific investment platforms that offer bonus incentives (Wealthsimple’s transfer match or banks offering points for a contribution, for example, as noted above). Though bonuses shouldn’t be the be-all and end-all of your decision-making processes, it is a nice little bonus, literally, to hopefully end up with a little extra cash or reward for completing your RRSP online. In other words, as a consumer, you can benefit from the competition in the online space.

So, in a nutshell, the online route wins for speed, comfort, and control. Sarah went from dreading the whole thing to realizing just how simple it was. Like everything, there are two sides to the coin. We also covered some potential barriers and caveats to watch out for.

Take Action Today for Peace of Mind

While navigating the Term Life Insurance approval process may feel overwhelming, it’s an essential step to securing financial peace of mind for your loved ones. Knowing what to expect and how long it might take can help alleviate the stress and also keep you in the loop through the process. If you are looking for an economical Term Life Insurance Plan in Brampton, Canada or want to get instant Term Life Insurance Policy Quotes Online, then take the help of an expert to make informed decisions with confidence.

If you’re ready to move forward, here are a few things you can do today to get started:

Assess Your Insurance Requirements:

Consider your family’s needs and what that translates to, how much coverage. If you are a bit lost, consulting with a seasoned insurance broker will clarify. You can explore Term Life Insurance Policy Quotes Online as well. This will give you an idea of alternatives and the cost of coverage. Take the time to make sure you won’t overpay for unnecessary coverage or under-protect your family.

Organize Your Medical Records:

Being prepared by having your medical history readily available can fast-track the approval process. Gather the required documents before applying. The required documents, which may include your recent medical history, prescriptions, and test results, should be gathered before applying. If you can be proactive in this area, then you can significantly reduce any delays.

Have an Insurance Broker’s Expertise On Your Side:

An experienced insurance broker like Canadian LIC can simplify the process. We can help you navigate through the complicated application process by making sure all required documents are in order and also ensure that you are getting the cost of Term Life Insurance Plan in Canada that fits into your budget. Brokers may also advise you on which insurers are most likely to offer you the best terms, considering your individual situation.

Compare Different Policies:

Do not take the quote that suits you the best. Devote time to search for different term life insurance policy quotes online. Premiums can vary widely, and it’s worth doing a bit of shopping around to make sure you’re getting the best deal that meets your needs. Shopping for policies also affords you the opportunity to hear about specific details about what is and isn’t covered.

Ensure your Application Remains Current:

After submitting your application, follow up regularly. Insurance companies may ask for further details or explanations. If you are on this early and participate in the process, it will go much faster.

Challenges and How to Overcome Them

Making an RRSP contribution online is nothing without its trials. The first step is being aware of them; the second is knowing how to counter them. Here are some of the most common problems people fear or face, along with advice for getting through each:

Security Breaches: The thought of one’s hard-earned cash whizzing through cyberspace can feel disconcerting. And although banks use robust security systems and encryption, it pays to be vigilant. Always confirm you’re on the official website (check for https:// and the padlock icon in your browser). Do not open links in unsolicited emails that claim to be your bank — those may be phishing scams. Instead, go directly to your bank’s site yourself or their official app. Also, use strong passwords (and two-factor authentication — a one-time code sent to your phone, for example — which most banks give you the option of having). This makes it very difficult for anyone else to access your active accounts. Raj, one of our clients, confessed he used to only bank in person out of security concerns. We had him turn on biometric login for his bank’s mobile app, and we showed him all the security guarantees that the bank makes. The fact that any reputable institution is federally regulated and typically insured (meaning that, in the worst-case scenario, his money was safe) made the switch to online transfers reassuring

Mistaking the Transfer: “What if I screw up?” That was one of the things Sarah worried about. The common mistakes could be sending money to the wrong account or contributing the wrong amount. Fortunately, most online banking interfaces are relatively intuitive. Takes it slow the first time so as not to make mistakes. Make sure you transferred to your RRSP (not, say, your TFSA or another account). Double-check the total — verbalizing it may help (like reading “five thousand dollars” as you look at $5,000 can prevent your eyes from hopping over an additional zero). And as mentioned in the steps, always check the summary prior to confirmation. If you happen to overcontribute, don’t sweat it. Tiny amount-over-contributions (within $2,000 naught the limits) aren’t note punished, but anything overhead that accrues 1% kind every month until removed CANADA.CA. If that happens, you can typically remedy the situation by withdrawing the excess amount or reaching out to that institution for assistance. One of our clients created two competing automatic contributions (whoops!) and then went over the $500 limit (whoops again), but noticed it a month later. With our help, he completed a T1-OVP notice for the excess contribution and withdrew the excess contribution. It was some paperwork, but all was well. The takeaway: check your contributions every once in a while (which is relatively easy to do online), and you’ll catch any problem before it escalates.

Investments Made Without Guidance: When you transfer online, and particularly if you transfer to a self-directed RRSP, you might sense that you’re all alone in deciding how to invest that money. In an in-person appointment, an advisor may recommend where you should direct your contribution (e.g., into a particular mutual fund or GIC). Online, you have plenty of options — which can be intimidating if you are uncertain about what to choose. The way to terminate this is to use the available resources. Most online platforms come with built-in tools or tutorials to help you select investments based on your goals and risk tolerance. Some banks have an “investment selector” or even allow you to chat with an advisor virtually. You can also take baby steps: there’s nothing wrong with, at least to begin with, making a contribution to an RRSP high-interest savings or a conservative fund until you know more. You can always change investments down the road. In fact, after transferring the money, Sarah called her bank’s investment helpline to discuss which fund to invest in. After 20 minutes, she decided on an RRSP moderate balanced fund. If you require that human touch, however, it’s there to find – even when you carry out the transfer online. Also, Canadian LIC is available to help, and many of our clients transfer funds online but are still consulted with us regarding overall RRSP planning and investment strategy.

Technical Glitches or Access Issues: Let’s be honest, no tech is 100% glitch-proof. The website is down just as you want to make a last-minute contribution, or your Internet sputters out at the most inopportune moment. These things can happen. Planning ahead is the best way to avoid panic. If you can, by all means, do not leave your contribution to the final day! But if you have to and nothing’s working, know that most institutions can process phone transactions as a backup (the wait times might be lengthy during RRSP season, but at least it’s an option). Also, there are a lot of banking apps and websites that allow future-dated contributions — so you could schedule your contribution ahead of time, a few days in advance of the deadline date, and then you don’t even have to log in on the day at all. In Sarah’s case, her initial transfer went through without any issues. But if the site had frozen, her plan B was to attempt the bank’s mobile app, and plan C was to call the customer service line to make sure her contribution got recorded anyway. Her backup plans provided her with some comfort around “What if the computer/internet fails me.”

Not Sure if Everything Went Through: Some people submit a transfer, then aren’t 100% sure it went. Did I do it right? If your RRSP lives at the same bank as your source account, you should see the new balance immediately (and probably receive an email notification). If it’s a transfer to another institution, you may see just money out of your bank account at first, which can be nerve-wracking until you see you’ve arrived in the RRSP. To avoid this problem, always verify the deposit to the RRSP account. External transfers can take a day or so, so don’t worry if it’s not instantaneous. Do save any confirmation numbers or screenshots. And in the extremely unlikely event that there’s something wrong, you’ve got the proof, and the institutions will track it down. In our experience, missing or misdirected contributions are extremely rare so long as you have entered all information correctly. And if you’re the nervy type, make your transfer a little early. So that you can check everything and rest easily.

In other words, online RRSP transfers are all about security, accuracy, and sometimes support. As long as you are vigilant (for security), attentive (for accuracy), and holistically proactive in seeking advice when appropriate, you can ultimately conquer these hurdles. By the end of the process, Sarah’s initial fears had gone away for the most part. She learned her best friends are knowledge and preparation. So, to close out with the big question she asked in the beginning: is transferring money into an RRSP online the right decision for you?

Conclusion: Is Transferring Money to an RRSP Online the Right Choice?

As Sarah’s story shows, in most cases, a transfer to an RRSP online in Canada is THE way to go. Weighing the pros and cons, here’s my take:

For most users, the benefits outweigh the drawbacks by far.

The ability to contribute when you want, knowing that you’ll get instant confirmation and that you’ll have full discretion over what you’re transferring. With busy lives, it’s invaluable to be able to “embrace digital banking with confidence” and do what you need to financially on your own schedule

And, with reputable institutions using high-level security protocols and insurance, the online process can be as safe as going into a branch (and often more convenient). For Sarah, once she grasped the process and saw it play out, she wondered why she hadn’t started doing it years ago. That said, whether it’s the right decision also has to do with your comfort level. If you’re tech-savvy or even just moderately comfortable online, you’ll probably consider this method empowering. If you’re still uncomfortable, that’s fine, too. You might begin with a small transfer or make an automatic contribution of a small amount just for practice. Use your bank’s online resources, or talk to an adviser (by phone or video chat) to guide you through the first time. And as you gradually learn how to manage the interface and begin to see successful outcomes, your confidence will build. A number of our Canadian LIC clients who were reluctant to make online contributions have now become regular users of online contributions after taking the plunge with some hand-holding.

So, is it a good choice? In a word, yes — with a few caveats. Yes, if what you’re looking for is flexibility and control over your finances. Yes, if you like the immediacy and clarity that digital tools offer. And oh, yes, if you care to get up to speed on the process and the safeguards (as Sarah did). The types of drawbacks – security concerns or making mistakes – can be mitigated by practicing good habits and taking advantage of the support available. On the one hand, however, if you have been around long enough to know that no matter how many conference calls you set and no matter how often you insist on going through this or that idea during regular progress check-ins, unless someone tells you you need to do something then you most likely aren’t going to contribute, then go with whatever method best supports you. What matters is that you routinely fund your RRSP.

Ultimately, there are all sorts of reasons why transferring money to your RRSP online is going to be the modern and convenient approach to taking control of your financial future. As Canadian LIC has found with its clients, once initial fears are calmed, nearly all embrace the online approach — and never look back. If you’re still not sure, maybe give it a shot at a small donation. You may well be one of the many Canadians who, after answering these questions, feel empowered and relieved to know that their retirement savings are a few clicks away — safe, sound and steadily growing for the future.

Remember: Whatever way you transfer money into an RRSP, online or in person, the key is you’re saving for retirement. The fact that you do it is more important than how you do it. But if online transfers do make that task more manageable and more accessible (as it did for Sarah), then it could be the right option for you, too.

More on Term Life Insurance

- Is RRSP Taxable?

- Can You Withdraw Funds from Group RRSP?

- How Do I Use My RRSP for Retirement?

- What Are Unused RRSP Contributions?

- Can You Transfer an RESP to an RRSP?

- Who Should Not Use RRSP?

- At What Age Should You Stop Contributing to RRSP?

- What is the Maximum RRSP Contribution for 2024?

- What Is RRSP & Reasons to Make RRSP Investments?

- What Should You Know About RRSP?

Get The Best Insurance Quote From Canadian L.I.C

Call +1 844-542-4678 to speak to our advisors.

Get Quote Now

FAQ: Transferring Money to an RRSP Online in Canada

Open your online banking or investment account, hover over your RRSP, and click “Contribute” or “Transfer.” Enter the amount and confirm. You’ll receive a receipt confirming your records.

Avoid over-contributing by checking your RRSP limit, ensuring you select the correct RRSP account, and double-checking the amount. Also, don’t forget to invest the funds once deposited.

Yes, online transfers are secure with encryption. Use strong passwords, enable two-factor authentication, and avoid public Wi-Fi to protect your personal information.

Yes, providers vary in fees, investment options, and customer service. Choose one based on convenience, fees, and the type of investment you want, whether it’s savings, stocks, or mutual funds.

Yes, many providers offer online tools to estimate your RRSP savings, tax refunds, and investment returns. It’s a good starting point to understand how much you could contribute or save.

Know your RRSP contribution limit, track your contributions, and stay under your limit. Contribute early, not last minute, to avoid missing the deadline or over-contributing.

Online transfers are faster, more convenient, and available 24/7. In-person transactions offer more immediate personal support but are limited to bank hours.

Use secure Wi-Fi, strong passwords, and two-factor authentication. Be cautious of phishing emails, and always verify you’re on the official website of your RRSP provider.

Big banks offer convenience and in-person service, while online brokers give you more control over investments at lower fees. Credit unions often offer competitive interest rates.

Consider fees, customer service, and the types of investments available. If you’re hands-off, go for a robo-advisor; if you prefer control, a self-directed RRSP is ideal.

About the Author – [Harpreet Puri]

Harpreet Puri is a seasoned financial expert and insurance advisor at Canadian LIC, specializing in retirement planning, investment strategies, and wealth protection solutions. With over a decade of experience in the Canadian financial sector, Harpreet Puri has helped thousands of individuals and families navigate the complexities of RRSPs, life insurance, and investment options tailored to their financial goals.

As a part of Canadian LIC—one of Canada’s leading insurance and investment brokerages, Harpreet Puri is dedicated to empowering Canadians with financial knowledge to make informed decisions about their future. Whether it’s understanding RRSP contributions, maximizing tax benefits, or selecting the right financial products, Harpreet Puri provides personalized guidance backed by industry expertise.

Harpreet Puri is committed to delivering client-centric financial solutions, ensuring that each individual receives the best investment and insurance advice aligned with their needs. This blog is a testament to [his/her/their] expertise, breaking down complex financial concepts into simple, actionable insights for Canadians.

Connect with [Harpreet Puri]:

- Website: [https://www.canadianlic.com/]

- LinkedIn: [https://www.linkedin.com/in/harpreetpuricanadianlic/]

Sources and Further Reading

- Government of Canada – RRSP Information

Official guide to RRSPs, including contribution limits and how RRSPs work. - Canada Revenue Agency – RRSP Contribution Limits

Learn how to check your RRSP contribution room and avoid over-contribution penalties. - Financial Consumer Agency of Canada (FCAC) – Understanding RRSPs

Detailed information about managing retirement savings and the different RRSP options. - TD Direct Investing – RRSP Investment Options

TD’s resources on how to manage and invest within a self-directed RRSP. - Wealthsimple – RRSP Overview

A robo-advisor platform that simplifies RRSP investment with automated investment options. - BMO – How to Use Your RRSP

BMO offers guidance on making RRSP contributions and managing retirement savings.

Key Takeaways

- Transferring Money to an RRSP Online is Easy and Secure:

Online RRSP transfers are convenient, fast, and secure when you use trusted providers. Always ensure you use strong passwords and secure Wi-Fi to protect your personal data. - Avoid Common Mistakes:

Double-check your RRSP contribution limit before transferring money to avoid over-contributing. Be sure to select the correct RRSP account and verify the transfer details before confirming. - Choosing the Right RRSP Provider:

Different providers offer varying fees, investment options, and services. Compare options like banks, online brokers, and robo-advisors to find the best fit for your needs. - Security Is Key:

Ensure you use two-factor authentication, avoid public Wi-Fi, and verify you’re on the official website of your provider to protect your financial information. - RRSP Contributions and Deadlines:

Contribute early to avoid last-minute issues and over-contribution penalties. Contributions made in the first 60 days of the year can count toward the previous year’s tax deduction. - Online Transfers Are Convenient:

Online RRSP transfers are available 24/7, allowing you to contribute whenever it fits into your schedule, without the need to visit a bank branch. - Keep Records:

Save your confirmation receipt and contribution details for tax purposes. Make sure you understand how your RRSP contributions affect your taxes and retirement planning.

Your Feedback Is Very Important To Us

We’d love to hear about your experience with transferring money to your RRSP online. Your feedback helps us understand any struggles or challenges you might face and how we can better assist you. Please take a few minutes to fill out the questionnaire below.

Thank you for your time and valuable feedback. We will use your responses to improve the experience for future users and assist you better in the future!

IN THIS ARTICLE

- Can I Transfer Money To RRSP Online?

- Getting a Registered Retirement Savings Plan Quote Online

- Comparing Registered Retirement Savings Plan Providers in Canada

- Registered Retirement Savings Plan Providers in Canada-Comparison

- Step-by-Step: How to Transfer Money to an RRSP Online

- Advantages of Transferring Money to an RRSP Online

- Take Action Today for Peace of Mind

- Challenges and How to Overcome Them

- Conclusion: Is Transferring Money to an RRSP Online the Right Choice?

Sign-in to CanadianLIC

Verify OTP