Think about being at a busy family gathering where everyone is laughing and telling stories about the good old days. In the middle of all the happiness, you see your niece, who is ten years old and wants to become an astronaut. The topic of the talk was how her parents seemed worried about how they would ever be able to save enough money for her education, given how much college costs. This makes you think—what if you start saving for her education?

Many of us find ourselves wanting to support the educational aspirations of a child who is not our own, whether they be a niece, nephew, family friend, or even a neighbor’s child. Many people want to know if they can start a Registered Education Savings Plan (RESP) in Canada for someone else’s kids. Without a doubt, the answer is yes, and the system works very well!

This blog will guide you through the steps and considerations for opening an RESP for a child who isn’t your own. With each section, you’ll find relatable stories and engaging dialogue that invite you to explore the benefits and the immense value of setting up an RESP, ultimately showing why Canadian LIC is your best partner in this journey.

RESPs: A Gateway to Education Savings

What is an RESP?

The Registered Education Savings Plan in Canada, better known by its acronym, RESP, is a financial vehicle through which anyone with a Social Insurance Number can set aside money as a savings plan or tax stock insurance in order to provide a sound financial basis to permit the beneficiary to pursue post-secondary education. So, it lets subscribers grow and invest in a child’s post-secondary future while enjoying the benefit of government grants and tax-deferred growth. Whether you are a parent, grandparent, or just someone who cares about the future of a child, the RESP is an extremely organized way to save money for a child’s education.

The Fear of Overstepping Boundaries

John, a dedicated uncle, always wanted the best for his niece, Emily. He was aware of the financial struggles Emily’s parents were experiencing and was thinking of setting up an RESP for her instead. However, he hesitated, fearing that his offer might be seen as overstepping familial boundaries. This is a common concern among relatives and friends who wish to contribute to a child’s education fund. The key is to approach the topic with sensitivity and understanding, ensuring that it’s seen as a supportive gesture rather than an intrusion.

How to Open an RESP for a Child Who Is Not Your Own

A Step-by-Step Guide

Opening a Registered Education Savings Plan (RESP) for a child who is not your own is a noble and thoughtful decision. It underscores your commitment to their future and can significantly ease their financial burden when they pursue higher education. Let’s delve deeper into each step required to set up this Savings Plan Insurance for Education, ensuring that you proceed with clarity and understanding.

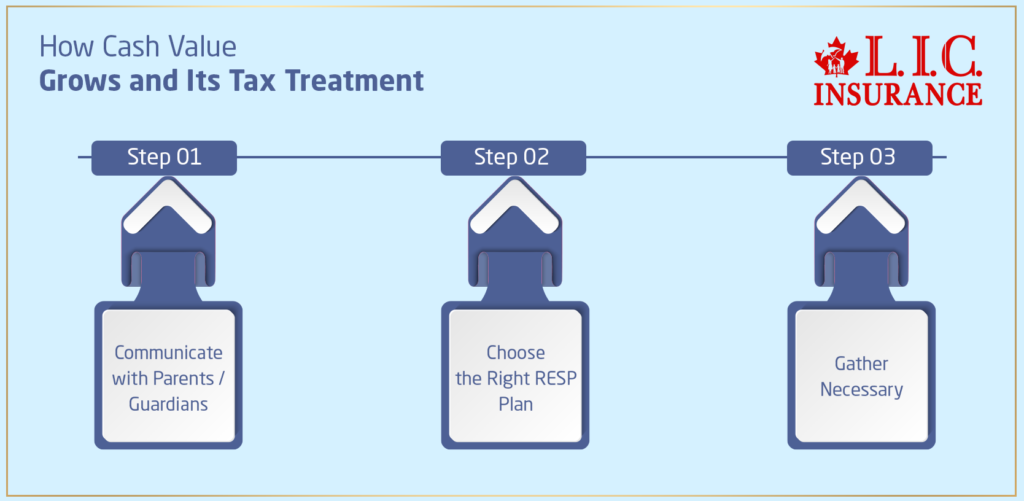

Step 1: Communicate with the Child’s Parents or Legal Guardians

The Importance of Initial Conversations

Before doing anything, one must have a heart-to-heart talk with the child’s parents or legal guardians. Take the example of Anita, who wanted to help her cousin Miguel, a young student. Knowing that Miguel’s parents were financially struggling, Anita saw the RESP as her chance to help Miguel positively influence his future. But she also understood the delicacy of providing financial assistance. She was able to strategically connect with the parents in a manner that mitigated threats to any negative assumptions by sharing how an RESP could benefit and support Miguel in his educational path.

Key Points to Discuss:

Explain your intentions clearly and the reason why you believe an RESP is a good idea.

Discuss the benefits of having a Registered Education Savings Plan in Canada, highlighting how it can grow and support the child’s academic journey.

Ensure that your gesture is seen as supportive, not as overstepping.

Step 2: Choose the Right RESP Plan

Selecting the Appropriate Plan

RESP plans are split into three categories: Family, Individual, and Group plans. The individual plan is the simplest and most direct option for the person who is not the parent of the child. This is a plan that enables you to contribute to an education savings plan for a child, even if you are not related to that child.

Understand the scenario of Lucy, an enthusiastic godmother to her friend’s daughter, Lisa. Lucy wanted to establish a RESP but was somewhat bewildered by the multiple types of plans she could open. After consulting with a financial advisor who provided her with an RESP Quote, Lucy opted for an individual plan, which suited her down to the ground because it would allow her to help one specific person (Lisa only), without stepping on the toes of any existing plans by any other family members of Lisa.

Things to Consider:

Determine whether a family or individual plan suits your situation best.

Understand the rules and benefits of each plan type, particularly how they handle contributions and withdrawals.

Step 3: Gather Necessary Information

Collecting Essential Details

After getting permission from the parents, the next step is collecting all the information required to establish the RESP. For instance, the child’s Social Insurance Number (SIN) must be obtained, as well as other necessary details like his or her date of birth and address. Those details are necessary for the RESP to be registered and to identify which government grants and bonds can be applied to the account.

Consider the experience of Thomas, who decided to open an RESP for his neighbor’s son, Kevin. Thomas had to ensure he had all the necessary documentation, which required coordinating with Kevin’s parents. This process reiterated the importance of maintaining open communication channels, as obtaining a SIN and other personal information is sensitive and must be handled with care and trust.

Documentation Required:

Child’s SIN.

Birth certificate or proof of identity.

Details about the child’s residency and citizenship status.

RESPs are community savings tools meant to create a well-supported development network for the younger generation, and they can and should be opened and offered without financial contributions as long as the person opening is truly committed to the child in question. As you ponder over this journey, recall the stories of Anita, Lucy, and Thomas. You, too, can change a child’s life in a great way, just like them. Ready for the next step and get a personalized RESP Quote? This is your opportunity to help make a child’s future brighter whilst getting a financial return on your donation with a long-term investment. Contact a trusted Canadian financial advisor today and begin a life-changing journey.

Maximizing the RESP: Grants and Benefits

Understanding Government Grants

One of the attractive benefits of the RESP is the Canada Education Savings Grant (CESG), which matches contributions of up to 20% on the first $2,500 contributed annually. That is up to another $500 a child per year of educational savings.

Missing Out on Grants

Emily’s parents initially set up an RESP but were not consistent with their contributions. When John took over, he maximized the contributions to ensure Emily received the full CESG each year, significantly boosting her education fund.

What Happens If the Child’s Post-Secondary Education Is Not Happening?

Options Available

Transfer the RESP: You can transfer the RESP to another eligible child without penalties, keeping the educational dream alive within the family or community.

Withdraw the Contributions: The contributions can be withdrawn by the subscriber without tax implications.

Flexibility in Planning

Mark, a neighbour who opened an RESP (Registered Education Savings Plans) for his friend’s daughter, found that she decided to start a business instead of going to college. Thanks to the flexibility of the RESP, he was able to transfer the funds to another child in the community who needed it for university.

Concluding Words

Starting an RESP for a kid who’s not your kid isn’t just a money thing, it’s this big vote of confidence in their future and dreams. The process is fraught with a lot of unknowns, but as you can see through many of the stories, the destination is worth it. By choosing Canadian LIC as your partner in setting up an RESP, you ensure that the process is smooth, the benefits are maximized, and your contribution truly counts towards building a brighter future for a child.

Do not allow another day to go by. Check out your RESP Quote and start your journey now with the best brokerage by your side—Canadian LIC. The steps you take today can clear a path for a child to succeed tomorrow.

Find Out: Can RESP be used for rent?

Find Out: The disadvantages of RESP

Find Out: The RESP Limit in Canada

Find Out: How to withdraw money from RESP?

Find Out: Does the beneficiary of an RESP need to live in Canada?

Find Out: How can you check your RESP in Canada?

Find Out Can an RESP be transferred to an RRSP?

Find Out: Important things about RESP in Canada

Find Out: Why to choose an RESP

Get The Best Insurance Quote From Canadian L.I.C

Call 1 844-542-4678 to speak to our advisors.

Frequently Asked Questions (FAQs) About Opening an RESP for a Child Who Is Not Your Own

Absolutely! You do not need to be a parent to contribute to an RESP to invest in a child’s future. Take neighbour Robert and his young science-loving friend, Alex. Robert knew that Alex’s family was poor in resources and burdened with worrying about how to manage it. Alex’s parents were happy to give him their blessing when they learned that he was going to put his money into a Registered Education Savings Plan in Canada. This is an excellen

Getting a quote is simple. You will have to provide basic information about the kid, like their name, birth date, and information on how much you aim to donate. When Maria chose to open an RESP for her niece, she called a financial advisor who would want that information and a number of other things, such as her own financial history, to come up with a personalized savings plan insurance. She found it very easy to use and was very happy with the clear, non-pressurizing advice she got.

Effective communication is an important aspect. It would help if you explained your goal and how the RESP will help you reach that goal. When James decided to set up an RESP for his grandson, for example, he had a conversation with his daughter about what he was going to do. They discussed the money, including government grants and the expansion of the investment. James took the time to explain to his daughter that this was an action of support and not an involvement in how they were handling their finances.

Consider the child’s unique situation. If you’re not a parent, then go with an individual plan. They are straightforward and focus solely on one beneficiary. Family friend Sandra, who wanted to contribute to her friend’s RESP for their son, discovered an individual plan was the best option for her. This left her free to make her own decisions about her own contributions without taking into account any other plans there might be for the child.

The limit per child per lifetime is $50,000. You have to remember this to escape from fines. Take the story of Eric, who enthusiastically started contributing to his goddaughter’s RESP without checking if other plans were already in place. After realizing he was close to exceeding the contribution limit, he coordinated with other family members to ensure they did not surpass the allowed amount, thus avoiding any unnecessary taxes or penalties.

The short answer is yes, you can experience substantial tax benefits. Although your contributions are not tax-deductible, the investment growth within the RESP is tax-free until it is withdrawn by the beneficiary and taxed at (presumably) a lower rate. Aunt Lisa opened an RESP for her niece because of this. She was glad to discover that her gifts were helping to create a tax-advantageous savings environment for the education of her niece.

You have options. The RESP can stay open for up to 36 years, giving the child time to determine that. If they decide not to continue their education after they turn 18, you can switch over the plan to another beneficiary or take the money back. When Tom encountered this situation with his nephew, he was able to transfer the funds to his younger niece, ensuring the family still benefited from his initial investment.

All of these questions give a glimpse into the key aspects of RESP investing for a non-biological child with the help of real-life stories that make the process more personal. By considering these stories and following these guidelines, you can make informed decisions that will greatly benefit a child’s educational future.

Sources and Further Reading

Government of Canada – RESP Official Page

URL: Canada.ca RESP

Description: This official government page offers the most authoritative and up-to-date information on RESPs, including details on how to open an RESP, the types of RESPs available, and how the government grants work.

Canada Revenue Agency – RESP and Grant Information

URL: CRA RESP Info

Description: The Canada Revenue Agency provides essential tax-related information on RESPs, including contributions, withdrawals, and the implications of over-contributing.

Employment and Social Development Canada – RESP Promoters

URL: ESDC RESP Promoters

Description: This page contains information for RESP promoters but is also useful for subscribers, as it covers the roles and responsibilities of those involved in managing RESPs.

Financial Consumer Agency of Canada – Choosing an RESP Provider

URL: FCAC Choosing an RESP Provider

Description: This guide helps you understand the different institutions that can offer RESPs and how to choose one that best fits your financial goals and the needs of the child.

GetSmarterAboutMoney.ca – RESP FAQs

URL: Get Smarter About Money – RESP

Description: Run by the Ontario Securities Commission, this site provides a straightforward Q&A format that covers common queries about RESPs, making complex topics more accessible to all.

By utilizing these sources, you will be well-equipped to make informed decisions about opening and managing an RESP for a child who is not your own, ensuring that you contribute positively to their future educational opportunities.

Key Takeaways

- Anyone can open an RESP for any child, enabling contributions to a child’s educational future by non-parents.

- Discuss your intentions with the child’s parents or legal guardians before opening an RESP to ensure transparency and cooperation.

- Individual RESP plans are typically most suitable for non-parents due to their straightforward nature.

- The lifetime contribution limit per child is $50,000, and utilizing government grants like the CESG can enhance savings growth.

- Contributions to an RESP grow tax-free, and withdrawals for educational purposes are taxed at the beneficiary's lower rate.

- Opening an RESP requires the child’s Social Insurance Number (SIN) and cooperation from the child's parents.

- If the child does not pursue higher education, the RESP can be transferred to another beneficiary or the contributions can be withdrawn without penalty.

- Opening an RESP demonstrates support and belief in a child’s potential beyond financial contributions.

- Readers are encouraged to open an RESP for a child not their own and consult a Canadian financial advisor for a personalized RESP Quote.

Your Feedback Is Very Important To Us

The above information is only meant to be informative. It comes from Canadian LIC’s own opinions, which can change at any time. This material is not meant to be financial or legal advice, and it should not be interpreted as such. If someone decides to act on the information on this page, Canadian LIC is not responsible for what happens. Every attempt is made to provide accurate and up-to-date information on Canadian LIC. Some of the terms, conditions, limitations, exclusions, termination, and other parts of the policies mentioned above may not be included, which may be important to the policy choice. For full details, please refer to the actual policy documents. If there is any disagreement, the language in the actual policy documents will be used. All rights reserved.

Please let us know if there is anything that should be updated, removed, or corrected from this article. Send an email to Contact@canadianlic.com or Info@canadianlic.com